So…what is a Dynasty Trust? It is an irrevocable trust designed to pass wealth through succeeding generations without incurring transfer taxes, like estate and gift taxes. A Grantor (person creating the trust) can currently pass $15M into a Dynasty Trust without paying any gift taxes. Once the assets have been transferred to the Dynasty Trust, they are no longer subject to estate or gift taxes regardless of how much the assets appreciate. A Dynasty Trust is typically set up to have no termination date, but to continue to hold the assets for the benefit of the Grantor’s lineal descendants forever.

Dynasty Trusts are a beneficial shareholder transition method in situations where fewer family members are working in the business, but where the traditional exit strategies, such as selling the family business or buying out family members not working in the company, are not consistent with the family’s mission, vision, and values. For example, family members may want to stay connected to the family legacy as a shareholder accruing the company’s economic benefit (i.e. dividends), but do not want to be involved in the day-to-day operations of the family business. In addition, the formation of a Dynasty Trust also reduces redemption pressure on the family business at the death of a shareholder to avoid an estate tax bill related to the illiquid family business asset without the liquidity needed.

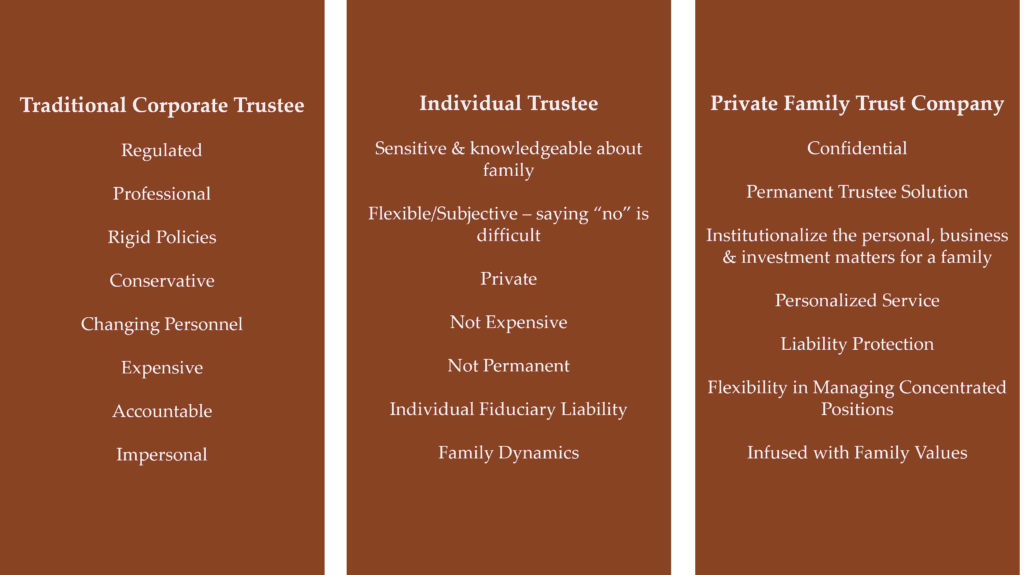

When establishing a Dynasty Trust, one of the considerations is not only who will serve as the current Trustee, but who the Trustee will be in the future. Grantors may have family members or advisors they are comfortable with serving today, but who will serve as Trustee for family members going forward? Traditionally, Trustee choices consisted of either a corporate trustee or an individual, frequently a family member. Having a Family Trust Company (“FTC”) serve as Trustee encompasses the best of both worlds, including positive characteristics of a corporate trustee and individual trustee.

Forming a FTC to serve as the trustee for a Dynasty Trust serves to institutionalize the personal, business, and investment matters for a family, while also preserving and instilling family values. FTCs offer a permanent trustee solution with personalized service, flexibility in managing concentrated positions, and liability protection.

From a Case Study perspective – consider the family with five siblings at the second generation (“G2”). Each G2 sibling owned shares of the family business and wanted to set up Dynasty Trusts to pass their shares to future generations. They quickly realized that each G2 sibling could select a different trustee. Each trustee could have a different perspective on the desired performance of the family business, have varying knowledge about the company and the family, and have a different perspective on their willingness to hold a concentrated asset in the trust. The impact of separate trustees could result in additional distractions to management at the family business, as the different trustees reach out requesting information or questioning management decisions. Instead, the family established an FTC with a Board consisting of Family Branch Representatives as well as some independent, trusted advisors. The FTC Board elects the Directors on the Board of the family owned business, as well as oversees the Committees responsible for directing the investing of any liquidity in the trusts, distributing assets from the trusts and providing educational programming to the beneficiaries family members. Through establishing a FTC to serve as Trustee of the family’s Dynasty Trusts, the family members remain the dominant voice in guiding the family and the family business across generations.

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as financial, tax or legal advice.